在Pandas DataFrame中推断值

Jim*_*y C 9 python pandas extrapolation

在Pandas DataFrame中插入NaN单元非常容易:

In [98]: df

Out[98]:

neg neu pos avg

250 0.508475 0.527027 0.641292 0.558931

500 NaN NaN NaN NaN

1000 0.650000 0.571429 0.653983 0.625137

2000 NaN NaN NaN NaN

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN

[12 rows x 4 columns]

In [99]: df.interpolate(method='nearest', axis=0)

Out[99]:

neg neu pos avg

250 0.508475 0.527027 0.641292 0.558931

500 0.508475 0.527027 0.641292 0.558931

1000 0.650000 0.571429 0.653983 0.625137

2000 0.650000 0.571429 0.653983 0.625137

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN

[12 rows x 4 columns]

我还希望它使用给定的方法推断插值范围之外的NaN值.我怎么能这样做呢?

tmt*_*prt 15

推断熊猫DataFrame小号

DataFrame可能是外推的,但是,在pandas中没有简单的方法调用,需要另一个库(例如scipy.optimize).

推断

通常,外推需要人们对推断的数据做出某些假设.一种方法是通过将一些通用参数化方程曲线拟合到数据以找到最佳描述现有数据的参数值,然后将其用于计算超出该数据范围的值.这种方法的困难和限制问题是,当选择参数化方程时,必须对趋势做出一些假设.这可以通过不同方程的试验和误差来找到,以给出期望的结果,或者有时可以从数据源推断出它.问题中提供的数据实际上不足以获得良好拟合曲线的数据集; 但是,它足以说明问题.

下面是外推的一个例子DataFrame用3 次多项式

f(x)= a x 3 + b x 2 + c x + d (等式1)

该通用函数(func())曲线拟合到每列上以获得唯一的列特定参数(即a,b,c,d).然后,这些参数化方程用于使用NaNs 推断所有索引的每列中的数据.

import pandas as pd

from cStringIO import StringIO

from scipy.optimize import curve_fit

df = pd.read_table(StringIO('''

neg neu pos avg

0 NaN NaN NaN NaN

250 0.508475 0.527027 0.641292 0.558931

500 NaN NaN NaN NaN

1000 0.650000 0.571429 0.653983 0.625137

2000 NaN NaN NaN NaN

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN'''), sep='\s+')

# Do the original interpolation

df.interpolate(method='nearest', xis=0, inplace=True)

# Display result

print ('Interpolated data:')

print (df)

print ()

# Function to curve fit to the data

def func(x, a, b, c, d):

return a * (x ** 3) + b * (x ** 2) + c * x + d

# Initial parameter guess, just to kick off the optimization

guess = (0.5, 0.5, 0.5, 0.5)

# Create copy of data to remove NaNs for curve fitting

fit_df = df.dropna()

# Place to store function parameters for each column

col_params = {}

# Curve fit each column

for col in fit_df.columns:

# Get x & y

x = fit_df.index.astype(float).values

y = fit_df[col].values

# Curve fit column and get curve parameters

params = curve_fit(func, x, y, guess)

# Store optimized parameters

col_params[col] = params[0]

# Extrapolate each column

for col in df.columns:

# Get the index values for NaNs in the column

x = df[pd.isnull(df[col])].index.astype(float).values

# Extrapolate those points with the fitted function

df[col][x] = func(x, *col_params[col])

# Display result

print ('Extrapolated data:')

print (df)

print ()

print ('Data was extrapolated with these column functions:')

for col in col_params:

print ('f_{}(x) = {:0.3e} x^3 + {:0.3e} x^2 + {:0.4f} x + {:0.4f}'.format(col, *col_params[col]))

推断结果

Interpolated data:

neg neu pos avg

0 NaN NaN NaN NaN

250 0.508475 0.527027 0.641292 0.558931

500 0.508475 0.527027 0.641292 0.558931

1000 0.650000 0.571429 0.653983 0.625137

2000 0.650000 0.571429 0.653983 0.625137

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN

Extrapolated data:

neg neu pos avg

0 0.411206 0.486983 0.631233 0.509807

250 0.508475 0.527027 0.641292 0.558931

500 0.508475 0.527027 0.641292 0.558931

1000 0.650000 0.571429 0.653983 0.625137

2000 0.650000 0.571429 0.653983 0.625137

3000 0.619718 0.663158 0.665468 0.649448

4000 0.621036 0.969232 0.708464 0.766245

6000 1.197762 2.799529 0.991552 1.662954

8000 3.281869 7.191776 1.702860 4.058855

10000 7.767992 15.272849 3.041316 8.694096

20000 97.540944 150.451269 26.103320 91.365599

30000 381.559069 546.881749 94.683310 341.042883

50000 1979.646859 2686.936912 467.861511 1711.489069

Data was extrapolated with these column functions:

f_neg(x) = 1.864e-11 x^3 + -1.471e-07 x^2 + 0.0003 x + 0.4112

f_neu(x) = 2.348e-11 x^3 + -1.023e-07 x^2 + 0.0002 x + 0.4870

f_avg(x) = 1.542e-11 x^3 + -9.016e-08 x^2 + 0.0002 x + 0.5098

f_pos(x) = 4.144e-12 x^3 + -2.107e-08 x^2 + 0.0000 x + 0.6312

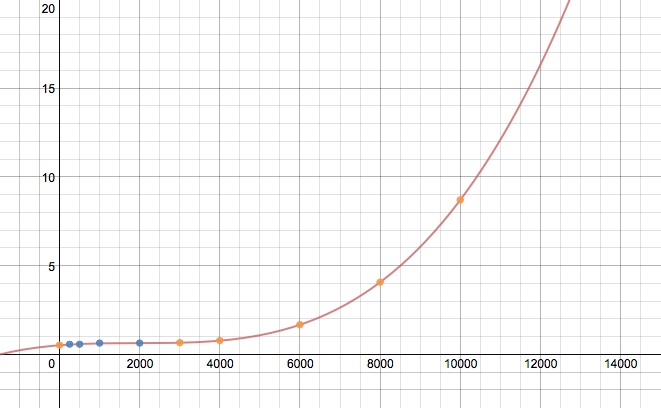

avg列的绘图

如果没有更大的数据集或知道数据的来源,这个结果可能完全错误,但应该举例说明推断a的过程DataFrame.在假设的公式func()可能将需要发挥与以获得正确的推断.此外,没有尝试使代码有效.

更新:

如果您的索引是非数字的,如a DatetimeIndex,请参阅此答案以了解如何推断它们.

import pandas as pd

try:

# for Python2

from cStringIO import StringIO

except ImportError:

# for Python3

from io import StringIO

df = pd.read_table(StringIO('''

neg neu pos avg

0 NaN NaN NaN NaN

250 0.508475 0.527027 0.641292 0.558931

999 NaN NaN NaN NaN

1000 0.650000 0.571429 0.653983 0.625137

2000 NaN NaN NaN NaN

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN'''), sep='\s+')

print(df.interpolate(method='nearest', axis=0).ffill().bfill())

产量

neg neu pos avg

0 0.508475 0.527027 0.641292 0.558931

250 0.508475 0.527027 0.641292 0.558931

999 0.650000 0.571429 0.653983 0.625137

1000 0.650000 0.571429 0.653983 0.625137

2000 0.650000 0.571429 0.653983 0.625137

3000 0.619718 0.663158 0.665468 0.649448

4000 0.619718 0.663158 0.665468 0.649448

6000 0.619718 0.663158 0.665468 0.649448

8000 0.619718 0.663158 0.665468 0.649448

10000 0.619718 0.663158 0.665468 0.649448

20000 0.619718 0.663158 0.665468 0.649448

30000 0.619718 0.663158 0.665468 0.649448

50000 0.619718 0.663158 0.665468 0.649448

注意:我改变df了一点,以显示插值与插入nearest不同df.fillna.(参见索引为999的行.)

我还添加了一行索引为0的NaN,以表明bfill()可能也是必要的.